As you approach the age of 65, you’ll be eligible for Medicare, the federal health insurance program designed to provide coverage to seniors. However, the program is complex, and it’s important to understand the different options available to you, especially the difference between Original Medicare and Medicare Advantage.

Different Types of Medicare

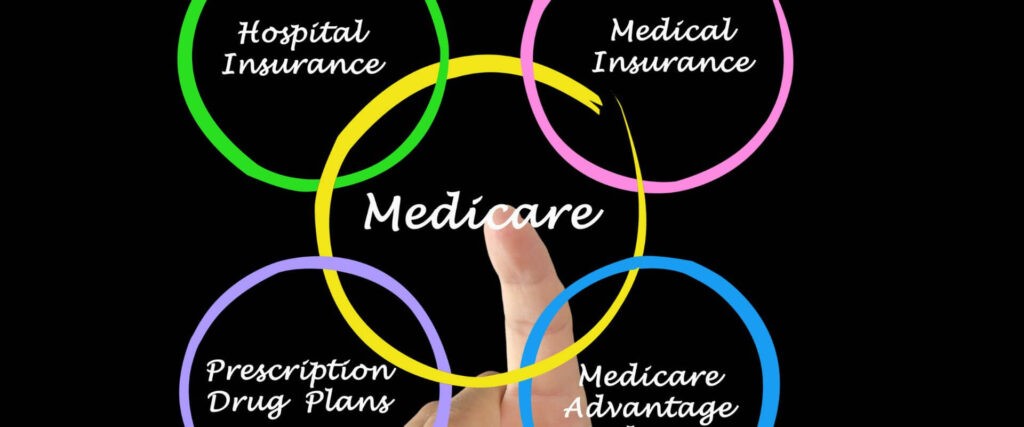

Original Medicare is the traditional Medicare program that consists of two parts: Part A (Hospital Insurance) and Part B (Medical Insurance). On the other hand, Medicare Advantage (also known as Part C) is a type of Medicare health plan offered by private insurance companies that contract with Medicare to provide all of your Part A and Part B benefits.

In this comprehensive guide, we’ll examine the key differences between Original Medicare and Medicare Advantage to help you make an informed decision about which plan is best for you.

Original Medicare

Original Medicare is the federal health insurance program for people who are 65 or older or have certain disabilities. It’s also available to people of any age with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a transplant) and Lou Gehrig’s disease. Original Medicare is made up of two parts: Part A and Part B.

Part A portion of the insurance coverage includes medical treatment provided in a hospital setting, including hospital stays, skilled nursing care, hospice services, and a selection of home health care options. On the other hand, Part B covers medical insurance, including services and supplies that are medically necessary to treat your health condition. That includes preventative services, ambulance transportation, mental health services, durable medical equipment, etc.

One of the key benefits of Original Medicare is its nationwide coverage. You can receive medical care from any doctor or hospital that accepts Medicare, regardless of where you live in the United States. Additionally, Original Medicare provides a comprehensive set of benefits, including preventive care, diagnostic tests, and treatment for a wide range of health conditions.

Medicare Advantage

Medicare Advantage, also known as Part C, is a type of Medicare health plan offered by private insurance companies that contract with Medicare to provide all of your Part A and Part B benefits. Medicare Advantage plans must cover everything that Original Medicare covers, but many Medicare Advantage plans also offer additional benefits, such as coverage for vision, hearing, dental, and gym memberships, wellness, etc.

Those plans typically have lower out-of-pocket costs than Original Medicare, but they also have restrictions on where you can receive medical care. Most Medicare Advantage plans have a network of preferred providers, and you’ll usually have to choose a primary care doctor and get referrals to see specialists (like with an HMO plan) If you receive medical care outside of your plan’s network, you may have to pay the full cost yourself. However, some plans like PPO, don’t require of beneficiaries to choose a primary care doctor nor seek referrals to see specialists. But, you will still pay higher out-of-pocket if you goo seek medical service outside your network.

One of the biggest advantages of Medicare Advantage is the potential for lower out-of-pocket costs. Most Medicare Advantage plans have a cap on your out-of-pocket expenses, meaning you won’t have to pay more than a certain amount for medical services in a given year (8300$ in 2023). Additionally, many Medicare Advantage plans include additional benefits, such as coverage for prescription drugs, which is not available with Original Medicare.

Cost Difference in Original Medicare vs Medicare Advantage

While Original Medicare has no monthly premium for Part A for most beneficiaries who have worked a minimum of ten years and paid Medicare taxes, you’ll typically pay a monthly premium for Part B. The cost of Part B varies depending on your income due to IRMAA, but the standard monthly premium in 2023 is $164.90.

With Medicare Advantage, you’ll typically have a monthly premium, alongside your Part B premium. You’ll also have to pay copayments, coinsurance, and deductibles for medical services, just like with Original Medicare. However, many Medicare Advantage plans have lower out-of-pocket costs than Original Medicare, and some even offer $0 monthly premiums. It’s important to compare the costs of both options and consider your individual health needs and budget when making a decision.

Prescription Drug Coverage Difference

Original Medicare does not cover prescription drugs, but you can enroll in a separate Part D Prescription Drug Plan to receive coverage. Part D plans are offered by private insurance companies and cover the cost of prescription drugs. You’ll pay a monthly premium for Part D coverage, and you may also have to pay a deductible, copayments, and coinsurance.

Many Medicare Advantage plans include prescription drug coverage, so you don’t have to enroll in a separate Part D plan. However, it’s important to check the details of your Medicare Advantage plan’s prescription drug coverage, as some plans may have restrictions on the drugs covered or require higher copayments for certain drugs.

Enrollment and Eligibility for Different Types of Medicare

To enroll in Original Medicare, you must be 65 or older, have certain disabilities, and be a legal resident of the United States. You can enroll in Original Medicare during your Initial Enrollment Period (IEP), which is the 7-month period around your 65th birthday. During your IEP, you can enroll in Original Medicare and add prescription drug coverage if desired.

If you don’t enroll during your IEP and decide to enroll later, you’ll face a 10% permanent increase in your Part B premium for each year that you were eligible for but not enrolled in Medicare. This means that if you wait two years to enroll, your premium could be 20% higher.

Here’s an example:

- Year 1: Not enrolled in Medicare during IEP, eligible for enrollment.

- Year 2: Not enrolled in Medicare during IEP, eligible for enrollment.

- Year 3: Enroll in Medicare, Part B premium is $164.90 + (10% x $164.90 x 2) = $164.90 + $33.98 = $198.88

You can also pay a late enrollment penalty for Part D if you don’t enroll when first eligible.

There are three enrollment periods for choosing or switching plans: the Initial Enrollment Period (IEP), the Annual Enrollment Period (AEP), and the Medicare Advantage Open Enrollment Period (OEP). AEP is from October 15 to December 7 and allows beneficiaries to change their coverage by switching to a different Medicare Advantage plan, Original Medicare, or changing their Part D prescription plan. The OEP is from January 1 to March 31 and allows beneficiaries enrolled in a Medicare Advantage plan to switch to another plan or return to Original Medicare. There is also a Special Enrollment Period (SEP) for beneficiaries who have Original Medicare but experience a qualifying life event. An Enrollment Period for qualifying life events and working past 65 provides a 2-month window for switching to a Medicare Advantage or Part D drug plan.

Key Differences Between Original Medicare vs Medicare Advantage

In conclusion, Original Medicare and Medicare Advantage are two distinct options for receiving Medicare coverage. Original Medicare provides comprehensive, nationwide coverage, while Medicare Advantage plans offer additional benefits and potentially lower out-of-pocket costs. When considering which option is best for you, it’s important to compare the costs, coverage, and benefits of each plan and consider your individual health needs and budget.

It’s also important to consider your lifestyle and travel habits when making a decision. If you frequently travel outside of the United States, Original Medicare may be the better option due to its nationwide coverage, and enrolling in Medicare Supplement plans can help you to cap out the foreign travel emergency costs. On the other hand, if you prefer lower out-of-pocket costs and are willing to receive medical care within a network of preferred providers, Medicare Advantage may be the better option for you.

It’s important to consult with a Medicare specialist or seek guidance from a trusted Medicare insurance agent or broker in order to make an informed decision about which option is best for you.